Within the 4Growth project, ongoing survey work across European observatories is building a comparative understanding of how digital technologies are being adopted in agriculture and forestry. This article presents early insights from the third wave of data collection conducted by the 4Growth Benelux Observatory, led by ILVO, combining 128 responses from Belgium and 10 from the Netherlands.

While the Belgian sample provides a robust basis for analysis, findings from the Netherlands should be interpreted as indicative due to the small sample size. Nevertheless, they offer a valuable snapshot of a region where digitalisation is advancing, yet not without structural challenges.

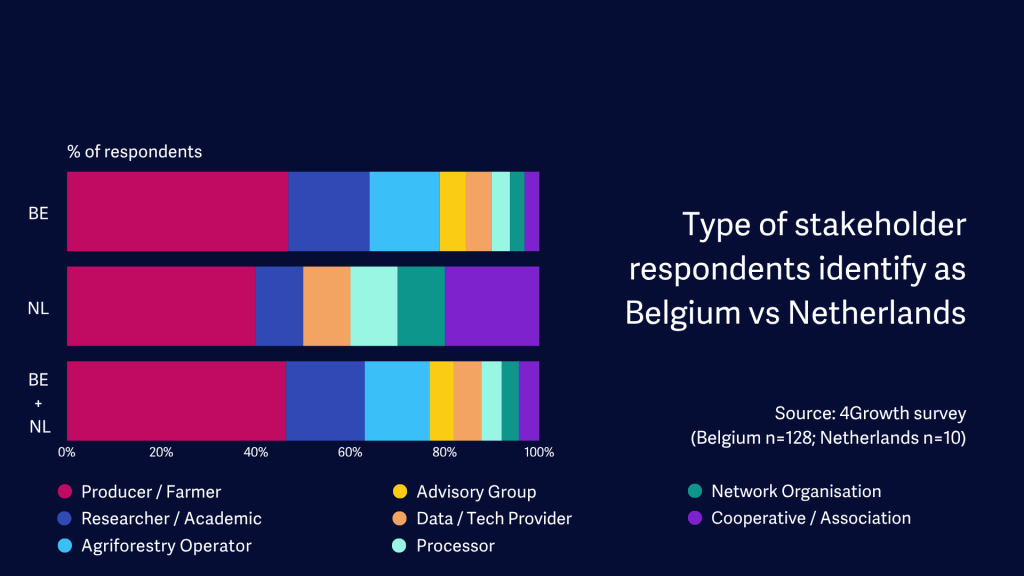

The Benelux Observatory captures a diverse set of stakeholders. Producers and farmers form the largest group, accounting for more than 46% of Belgian and Dutch respondents, followed by research and academic organisations, agri/forest operators, and advisory groups. This distribution reflects the 4Growth observatory approach, bringing together the full value chain.

Notably, around 75% of respondents work in micro-organisations with less than 10 employees, highlighting the dominance of small-scale and family-run structures, particularly in Belgium.

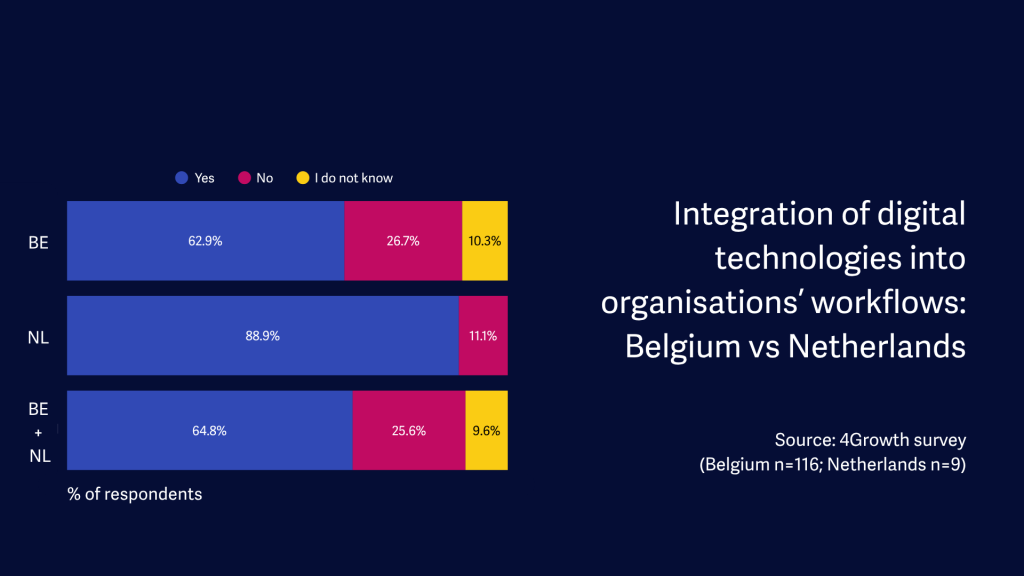

Digital technology uptake is already well established across the region. Overall, around 65% of respondents report that digital tools are integrated into their operations. Belgium aligns closely with this average (63%), while the Netherlands shows a notably higher adoption rate (89%).

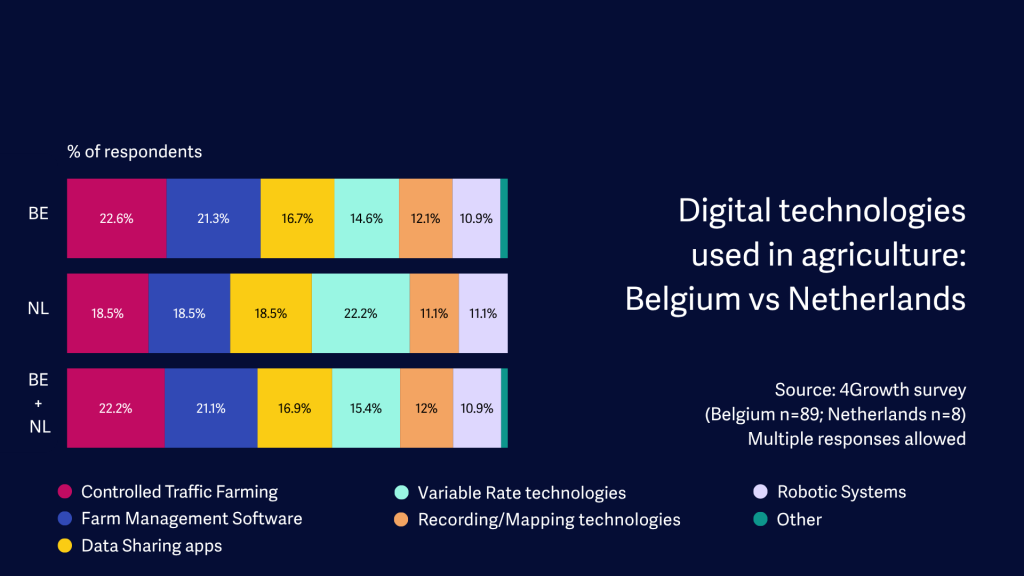

Across the region, Controlled Traffic Farming (e.g. GPS steering) and Farm Management Software are the most widely used technologies, representing around 23% and 21% of all selected technology options respectively. Data sharing apps follow at around 17%, reflecting a growing interest in data-driven collaboration across the value chain.

In the Netherlands, Variable Rate technologies are more prominent (approx. 22% of responses vs. 15% in Belgium). This suggests a more advanced uptake of precision agriculture applications that automate inputs such as fertiliser or chemical plant protection products based on sensor or remote sensing data for Dutch farmers.

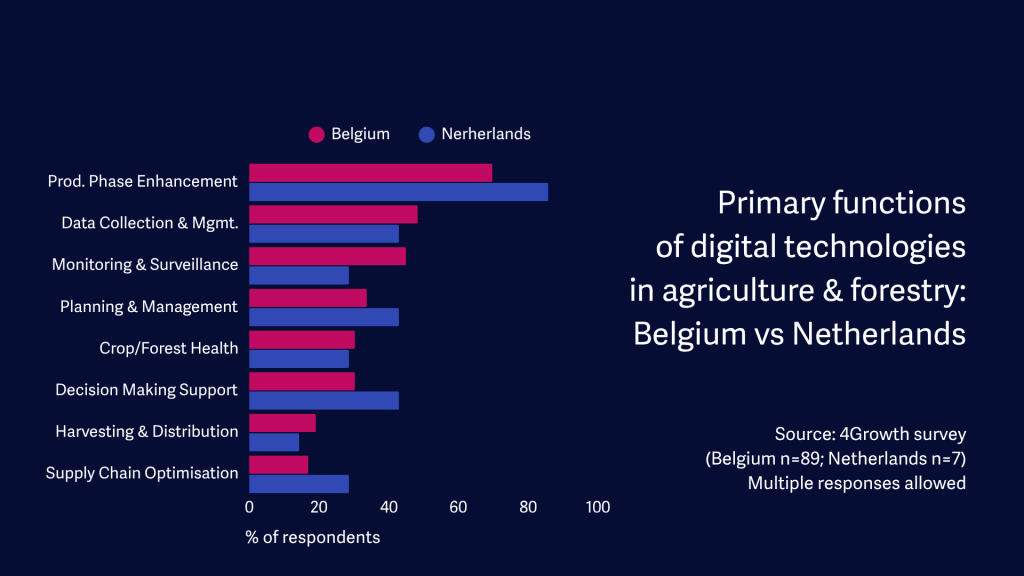

Production phase enhancement, referring to optimising yields and resource efficiency, is by far the dominant functional purpose of digital technologies, cited by around 70% of Belgian and 86% of Dutch respondents. Data collection and management and monitoring and surveillance round out the top three in combined results for Belgium and the Netherlands

However, differences emerge in how technologies are applied. Dutch respondents place considerably more emphasis on decision-making support (43% vs. 30% in Belgium), suggesting higher integration of AI and analytics-driven advisory tools in the Netherlands. Belgium scores notably higher on monitoring & surveillance (45% of Belgian respondents vs. 29% in the Netherlands) prioritising digital tools for crop health monitoring and pest detection, applications increasingly relevant to integrated pest management and the EU Farm to Fork strategy.

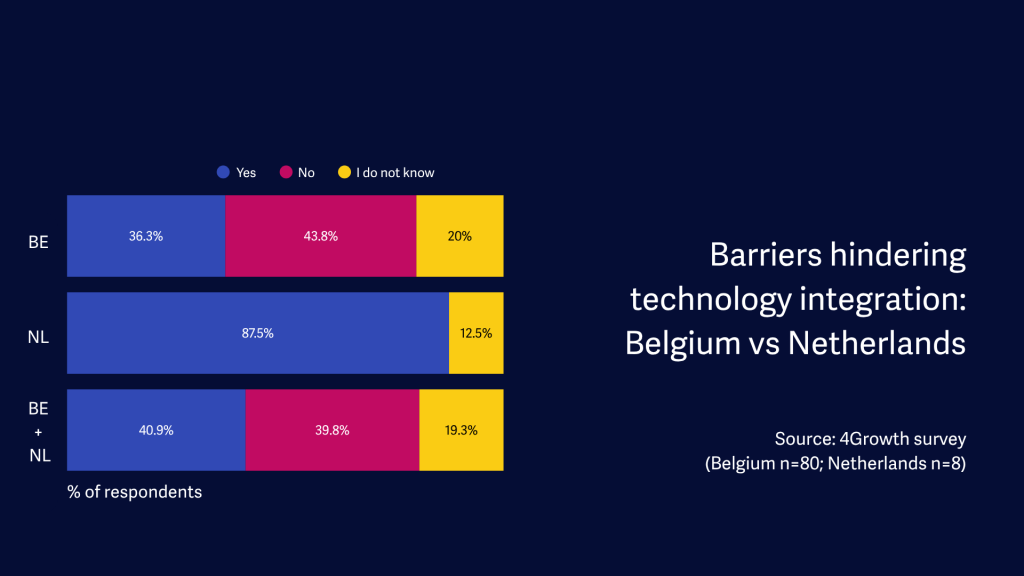

Despite high adoption rates, barriers are real and widespread. Across the region, around 41% of respondents report experiencing barriers to digital technology adoption. In Belgium this is reported by 36%. However, this rises sharply to around 88% in the Netherlands, despite the highest adoption rate reported there. This paradox reflects that early adopters encounter the friction of integration and interoperability firsthand.

Common barriers are identified across both countries. High costs and uncertain returns on investment remain key concerns, particularly for smaller operators, while interoperability issues make it difficult to connect systems and data streams. The lack of common data standards further limits scalability, and regulatory requirements, especially around data privacy and drone use, add to complexity.

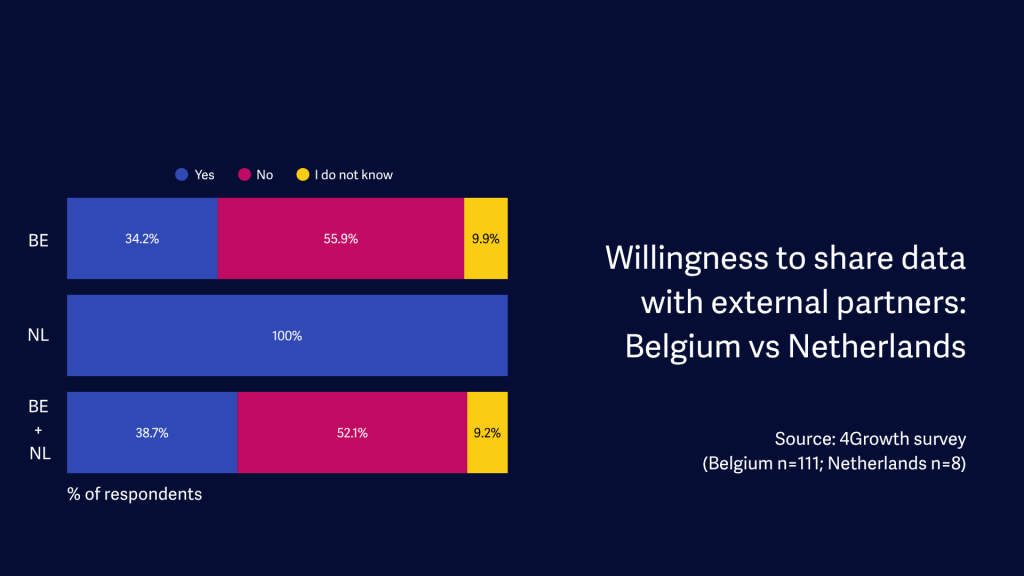

One of the most striking findings in wave 3 relates to data sharing practices. While all Dutch respondents (100%) report sharing data with external partners, only 34% of Belgian respondents do so. Even if the Dutch sample is small, the gap is noteworthy, especially given the existence of established data sharing initiatives in both countries (DjustConnect in Belgium and JoinData in the Netherlands). This may reflect differences in cooperative culture, trust in value chain partners, or the maturity of data-sharing infrastructure requiring further investigation in future survey waves.

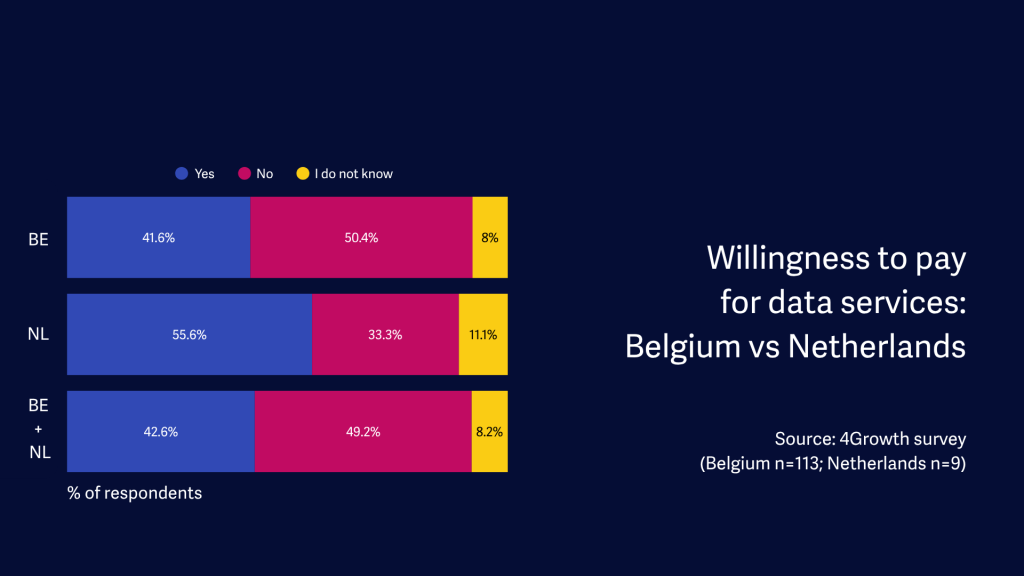

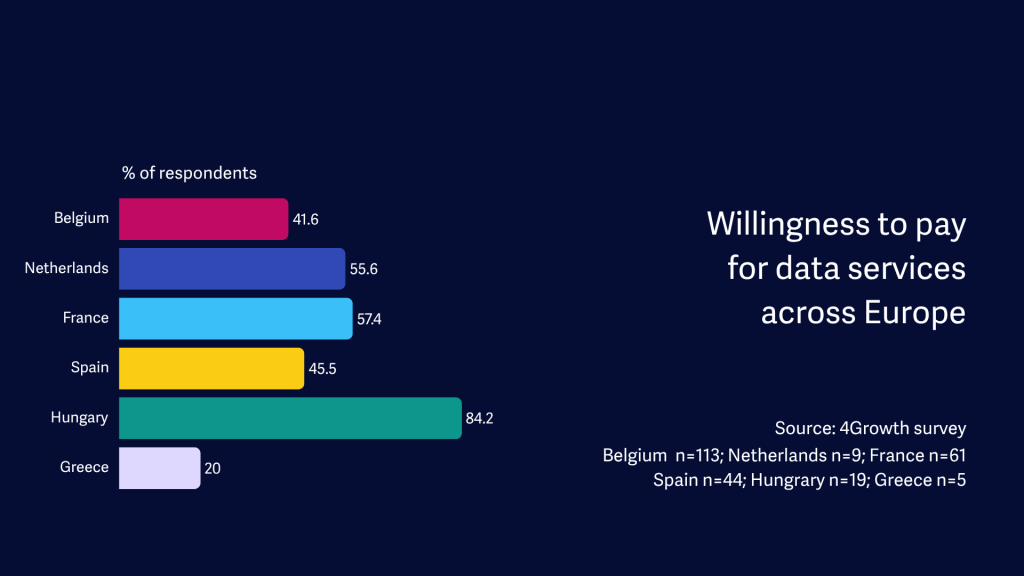

The willingness to pay for digital data services remains moderate in both countries (42% in Belgium, 56% in the Netherlands). This indicates that monetisation models for agricultural data services still need to mature to unlock broader commercial uptake.

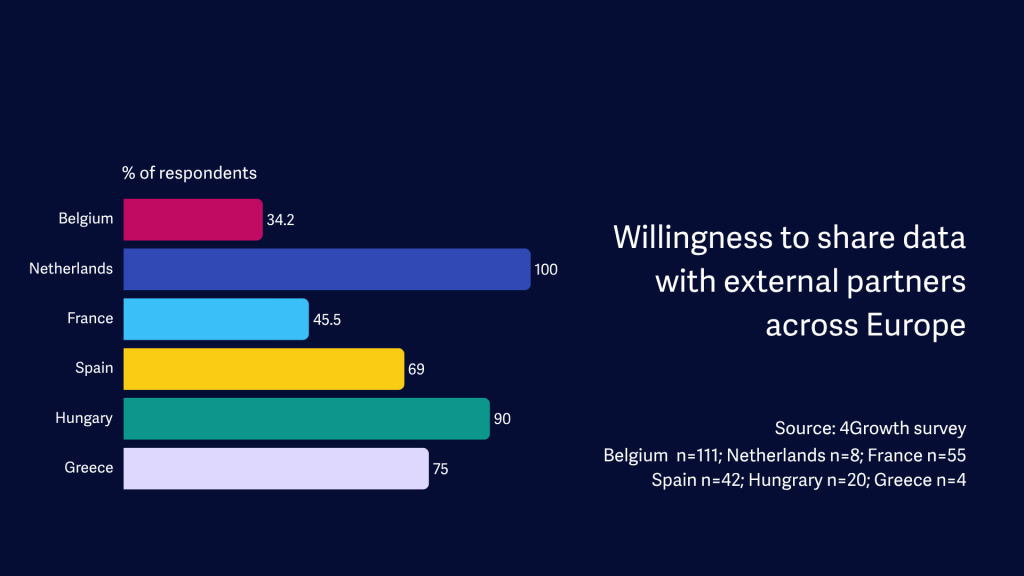

In comparison to other countries, measured in wave 3, Belgium shows the lowest level of data sharing, a noteworthy result as several efforts are ongoing to support farmers and other agrifood actors to start sharing their data in the country. While there are several countries with few answers in this wave, this raises interest for further investigation.

Findings from the Benelux Observatory confirm that digital transformation in agriculture is well underway, but the journey is uneven. While Belgian and Dutch stakeholders share similar technology portfolios, they differ in data sharing culture, specific technologies prioritised, and in barriers they face.

Cost, interoperability, and data standards remain key bottlenecks in both countries. Addressing these issues will require coordinated efforts across the value chain, from technology providers and cooperatives to policy makers and research organisations.

4GROWTH will continue to monitor these trends through additional survey waves and deepen the analysis with qualitative case studies. The full Wave 3 dataset, covering all 7 observatory countries, will be published later in 2026. Insights from the Observatories are progressively made available through the project’s Visualisation Platform, enabling stakeholders to explore and compare results across countries.

Sign up to stay informed of news, key outputs and upcoming events!